The Digital Dollar project is a study to implement a possible US CBDC (Central Bank Digital Currency). The study does not represent an official FED position but is a joint effort of a non-profit company (the digital dollar project: https://www.digitaldollarproject.org/) and Accenture, yet we are confident that it will greatly influence a potential U.S. CBDC realization. The digitized dollar would act as an official currency in addition to, but not in competition with, the currencies currently in use. Digitized dollars could be converted into paper dollars or equivalent account money, among other things, targeting the following major uses:

- Retail: To support financial transactions between individuals, commercial units and companies, complementing existing credit card and Clearing House's Electronic Payment Network (EPN) systems.

- Wholesale: To implement transactions between banks and other financial institutions, supplementing or even replacing Fedwire, National Settlement Service (NSS) solutions.

- International: To support international financial transactions.

In terms of implementation, it is not a question of complementing existing financial systems, but of designing a new financial infrastructure. This is also conceivable with distributed general ledger technology by incorporating AML / KYC requirements into the associated digital wallets.

Two independent dimensions are usually taken into account when implementing digital central bank money.

Based on the structure of the CBDC, it can be:

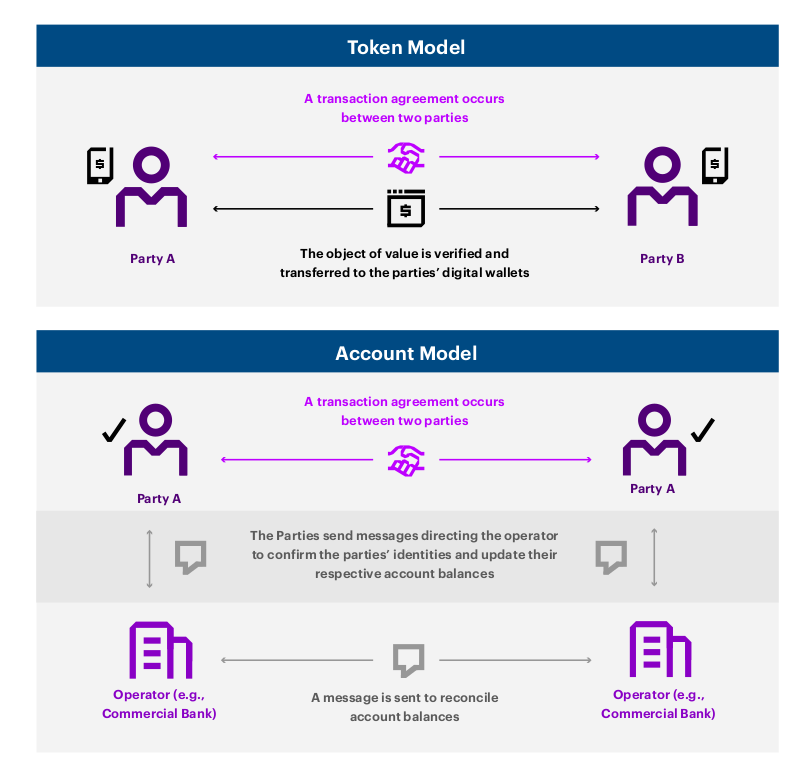

- Account-based: in this implementation, each user would create an online account with the central bank, similar to a normal bank account. However, the advantage of the solution, its simple feasibility, but its disadvantage is that the central bank would have to issue end-user accounts, which does not necessarily cut its profile, on the other hand, it would be a direct competitor to commercial banks.

- Coin (Token) based: here the CBDC would be implemented using digital coins issued and withdrawn by the central bank, either directly or indirectly through financial institutions to economic agents. In monetary terms, the system is similar to paper money-based systems and requires more, but with a good chance, new financial infrastructure (eg blockchain). However, token-based systems are expected to have several advantages over account-based systems, e.g. decentralization, flexibility, greater security and privacy. The US CBDC would be basically built on a token basis, the main reason being that it would ensure the smoothest possible transition between the current financial structure and digital central bank money.

Regarding the structure of CBDC, two main models are known:

- Single-tier: here, the central bank is in direct contact with all economic agents, either by keeping their accounts or by issuing them with digital coins. The disadvantage of this solution is that, as the central bank emerges as a direct competitor to commercial banks, it could cause a restructuring of the entire financial sector, which could significantly shake up overall financial stability.

- The tiered system would reflect the current institutionalized financial hierarchy, where the central bank would provide CBDC services to economic actors not directly but through other financial institutions.

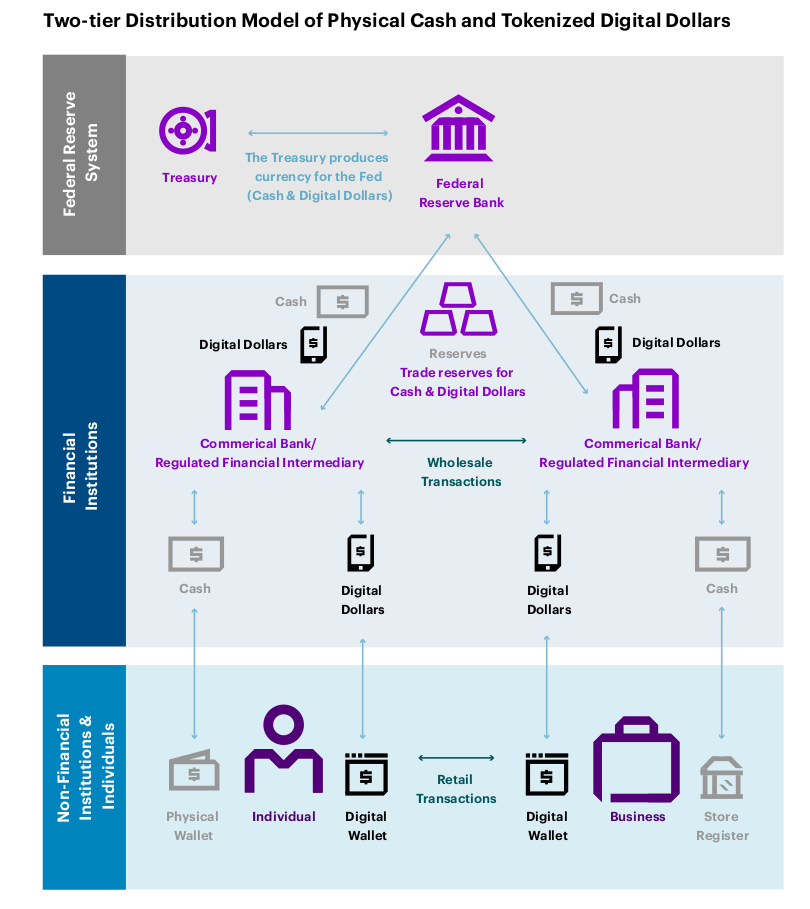

The following figure shows a possible digital dollar implementation with token-based digital dollar issuance and a tiered structure that would build on the current banking system in a similar way to the current dollar-based two-tier banking system:

- The Fed controls the monetary policy, issuance and possible withdrawal of the digital dollar.

- The digital token issued will first be received only by qualified financial institutions, which guarantee further distribution.

- At the end-user and retail level, the system would work like cash, apart from being completely digital, of course: Individual actors would be able to exchange value with a purely digital wallet, in a P2P way, ie without any institutional involvement.

There are no proposals or roadmaps for concrete implementation yet, so it is not certain that this will happen in the short term. However, if implemented, the ideas and architectural elements mentioned above will be an integral part of the digital dollar.