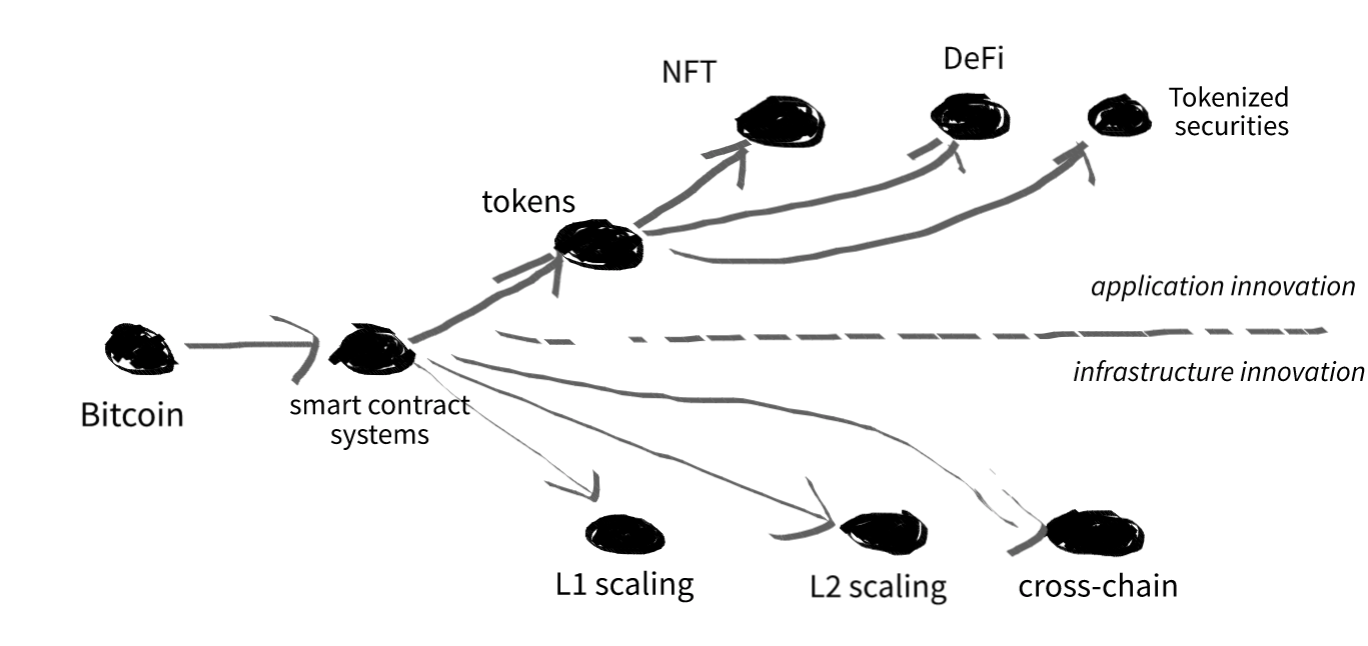

Current trends in blockchain research and development can be separated into two major categories. On the one hand, there is a very active research on the infrastructure side of these systems focusing mostly on scalability, privacy issues or cross-chain compatibility solutions of different distributed ledger platforms. Major approaches are layer 1 and layer 2 scaling possibilities. On the other hand, there is very active innovation on the application side as well having tokenization as a basic application level building block. Two of the probably well-known and perhaps over-hyped directions of the last 3 years are the NFT-s (non-fungible tokens) and DeFi (decentralized finance). As these approaches were mostly realized in the public and sometimes crypto-anarchist blockchain space, a lesser known direction on the regulated field is the trend of tokenized financial securities.

Tokenized financial securities are a new development in the financial industry that involves the use of blockchain technology to issue and manage securities in a digital form. These securities are represented by digital tokens that are secured and managed on a blockchain network. Tokenized financial securities are digital assets that represent ownership in a financial instrument, such as stocks, bonds, green-bonds, or real estate. They are issued through a process known as tokenization, which involves converting the ownership rights of an underlying asset into a digital token on a blockchain network. These tokens are then traded on digital asset exchanges or stored in digital wallets, just like other cryptocurrencies.

It is important to point out the difference between security tokens and tokenized securities. Security tokens are usually innovative and blockchain native tokens that are considered by the current legislation attempts under the same law as financial securities. It is especially difficult and controversial for native blockchain tokens and most of the decentralized finance (DeFi) protocols. However tokenized financial security considers classical financial securities that already exist for decades with well established regulation. These classical financial instruments are brought to blockchain protocols in a tokenized form.

One of the key benefits of tokenized financial securities is their potential to increase market liquidity. By enabling the fractional ownership of assets, tokenization allows investors to buy and sell smaller portions of assets, which can increase the number of potential buyers and sellers in a market. This can lead to more efficient price discovery and lower transaction costs. Tokenization also offers greater transparency and security than traditional financial securities. Since tokenized securities are recorded on a blockchain network, all transactions are transparent and immutable. This means that investors can easily track the ownership and transfer of securities, reducing the risk of fraud and errors. Furthermore, tokenization can help to reduce the cost and complexity of issuing and managing financial securities. By using blockchain technology, the process of issuing and trading securities can be streamlined, reducing the need for intermediaries and lowering transaction costs. This can make it easier and cheaper for companies to raise capital, and for investors to access a wider range of investment opportunities.

However, there are also challenges and potential risks associated with tokenized financial securities. One of the main challenges is the lack of regulatory clarity around these new digital assets. While some countries have established regulatory frameworks for digital assets, many others have not, creating uncertainty and potential legal risks for investors and issuers. Additionally, the adoption of tokenized financial securities is still in its early stages, and there are concerns around the scalability and interoperability of blockchain networks. As more assets are tokenized and traded on these networks, there is a risk that they may become congested, leading to slower transaction times and higher costs.

Major categories for tokenized financial securities are:

- Tokenized stocks: Companies can issue tokenized versions of their stocks, allowing investors to buy and sell them on a blockchain-based platform. This provides a more efficient and transparent way to trade stocks, with lower transaction fees and faster settlement times.

- Tokenized bonds: Similar to tokenized stocks, companies can issue tokenized versions of their bonds, allowing investors to purchase fractional ownership of the bond. This provides a more accessible way for investors to participate in the bond market.

- Tokenized real estate: Real estate assets can be tokenized, allowing investors to buy and sell fractional ownership of the property. This provides a more liquid and transparent way to invest in real estate, with lower transaction fees and faster settlement times. One interesting and perhaps controversial direction might be the tokenization of mortgage back securities (MBS) or asset backed securities (ABS) providing a more transparent and possible risk-free approach for the whole industry

- Tokenized commodities: Commodities like gold and silver can be tokenized, allowing investors to buy and sell fractional ownership of the asset. This provides a more accessible way for investors to participate in the commodity market.

- Tokenized funds: Investment funds can issue tokens representing ownership in the fund, allowing investors to buy and sell fractional ownership. This provides a more efficient and transparent way to invest in funds, with lower fees and faster settlement times.

In the international examples, we can already find several initiatives for the successful issuance of tokenized securities. An example of this is the tokenization of the BNP Paribas (BNPP) green bond. In the process, short-term tokens representing bonds were issued on the Ethereum blockchain. For the purchased tokens, the issuing institution undertook to officially convert them into the corresponding bond within 48 hours. Another example is Sygnum bank, which provides tokenized securities services to its customers. With its help, during a classic IPO, the issued shares can be listed on the Singapore Digital Exchange in parallel, in tokenized form. As a third example, it is perhaps worth mentioning Quadrant Biosciences, which sold 17% of its entire ownership in tokenized form. Another similar interesting direction is the tokenization of government securities, for which an innovative initiative will be launched in Israel at the beginning of next year, for example, with the support of the Tel Aviv Stock Exchange. Last but not least it is worth mentioning Siemens issuing a digital corporate bond in tokenized form just a couple of weeks ago.

Perhaps the question may arise as to how technically feasible a blockchain, especially public blockchain based securities issuance. The fact that most public blockchains are open, transparent, and accessible to everyone does not fit well with securities regulation. However, it is worth noting that, on the one hand, tokenization does not necessarily have to be implemented on an open blockchain platform, consortium platforms are conceivable, which can be regulated much better. On the other hand, even the most public and open platforms have token standards that can be used to create highly regulated tokens. Such a standard is, for example, ERC-1404, which enables, for example:

- know your token holder and KYC policies,

- linked to add KYC documents,

- whitelisting, blacklisting,

- blocking a token account,

- approving or prohibiting token transfer,

- “hard” coded rules: for example to prohibit trading between regions,

- token withdrawal,

- rights and roles (e.g. investor, administrator), etc.

In conclusion, tokenized financial securities represent an exciting new development in the financial industry, with the potential to increase market liquidity, transparency, and efficiency. However, there are also challenges and risks associated with this new technology, including regulatory uncertainty and scalability issues. As the adoption of tokenized financial securities continues to grow, it will be important for regulators, investors, and issuers to work together to ensure that these digital assets are safe, transparent, and accessible to all.