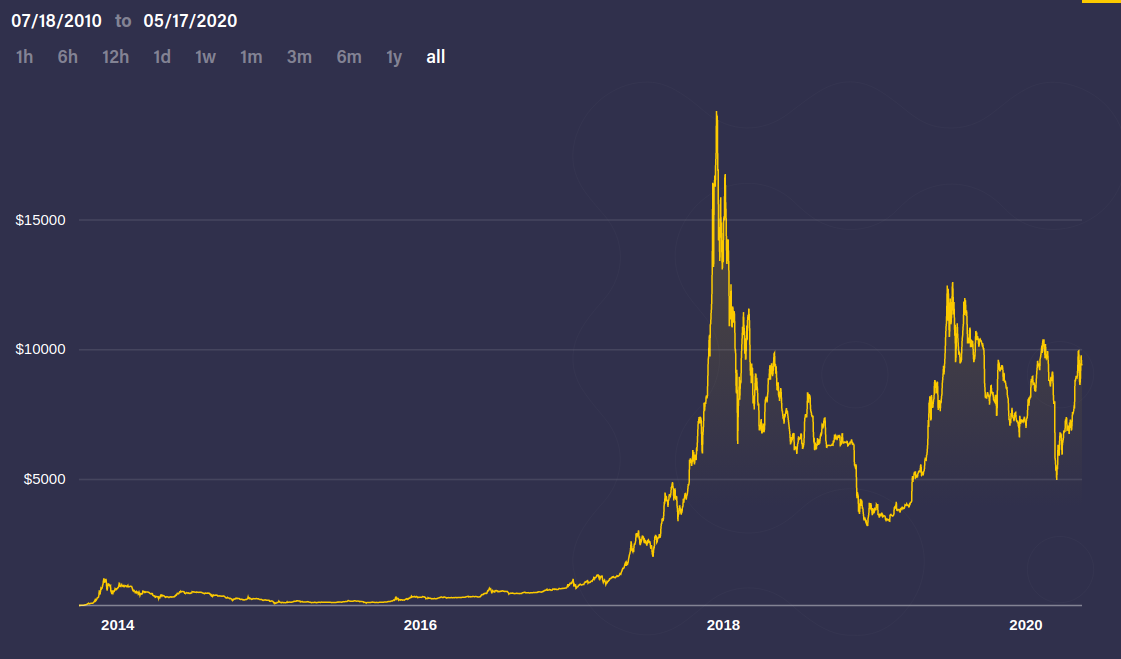

Anyone who has been dealing with blockchain and cryptocurrency technologies for a couple of years may still remember the market crash in 2018 and the one and a half year crypto winter that followed. The situation is well reflected in the bitcoin exchange rate shown in the figure below. Of course, the volume of the total kritpo and blockchain market is much larger than the current price of Bitcoin. However, since Bitcoin is used in most places as an interface crypto currency to enter and exit the crypto world, the chart below also shows the general cryptoconditions in 2018 quite well.

The Bitcoin price from 2014 to nowadays

First of all, it is important to note that we believe the blockchain is basically a transformative exponential technology. Exponential technologies have been evolving slowly for quite some time, and then, after a while, reaching their exponential stage, they are being used at an ever-accelerating rate (Figure 2). One of the best examples of this is artificial intelligence, and machine learning. If we consider only the backpropagation algorithm in the narrower sense as the birth of the area, the area has been in existence for more than 45 years. Nevertheless, we are not yet there for self-driving cars to travel on the roads on a daily basis, but it is conceivable that we will reach it within 5-10 years. This means 50-60 years until the technology reaches its true exponential stage, where it will actually result in radical innovations. Blockchain algorithms have been around for about 10 years. We believe that this technology will reach its exponential stage faster than artificial intelligence, but it may still take 10 to 20 years.

Life cycle of an exponential technology

On the other hand, general human thinking tends to underestimate the impact of a technology, especially if it is exponential: we tend to overestimate the effects in the short run, while we underestimate the effects in the long run. This is probably due to the structure of the human neocortex, which specializes in pattern recognition that is basically close to linear, so it also tries to approach an exponential change linearly. From another approach, the high level of media attention in the area caused a problem. With fundamental long-term technological change, the media tends to go to extremes: for example, to advertise something as a world-saving technology for half a year, and then, if it doesn’t change the world in six months, to declare it unusable.

Another feature of blockchain technology is that it is an infrastructure financial technology. In this respect, it is somewhat different from a simple fintech application that tries to save the world with a fancy mobile app and some business logic. It is more like classic infrastructure technologies such as the highway from which a few thousand kilometers have to be built in order for other applications to run on it, such as cars, trucks, motorcycles, and so on.

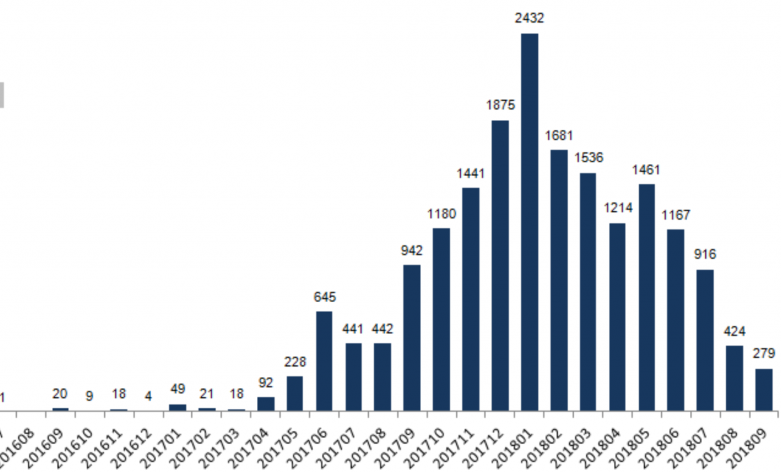

In 2015-16, a new application related to blockchain technology, called token sales, appeared, the earliest form of which is ICO (Initial Coin Offering, Figure 3). Token sales as a technology has fundamentally liberalized the investment market, both on the demand and supply side:

- On the demand side, it provided a new opportunity for any investor to acquire a stake in a startup starting up anywhere in the world on a basis of up to a few dollars.

- On the supply side, it provided an opportunity for a startup to raise funds from anywhere in the world, even in crowdfunding style in the form of individual investments of a few dollars.

In this sense, the problems arising from the short-term perception of the aforementioned exponential technologies have intensified even more than usual. Simply put, the blockchain is a technology that can implement its own financing as well.

Number of ICO-s around 2018

The biggest problem with ICO technology has been the complete lack of regulation in specific business implementations (and in some places this is not fully clarified today). This did not cause too much of a problem in the initial period of 2015-16, as it was mainly serious professional projects that carried out token sales, and since the technology was not very well known, mainly professional investors could be found in the market. By 2018, however, this has changed as a result of both the press publicity and the incredible exchange rate gains of the first successful projects:

- From the investor's point of view, investors who were not so much interested in technology or in the long-term success of a platform, but only in short-term exchange rate gains, began to dominate.

- As it was seen that there is quite a lot of “free money” in the market, startups have started to raise funds irresponsibly. Of course, there were also teams that did some serious project and teams that didn’t want to do anything just put away the funding they collected. However, most of the attempts were somewhere in between: since the funding was free, many tried to implement a project without worrying too much about whether there was or would be a specific market demand for it.

Overall, we believe that the factors mentioned above are:

- the beginning of the technological curve

- increased media attention and unrealistic expectations

- a liberalized investment market and "free money" without any regulation or control

they themselves have created an unsustainable market, inevitably creating an investment bubble.

The final push for a concrete market collapse was caused by a total regulatory fire that hit the ICO market in early 2018, but without it, the aforementioned scheme would probably not have been sustainable for a long time. The market crash was followed by a one and a half year crypto winter, causing significant difficulties for downsized and blockchain companies that incorrectly assessed market demand for their products, either because they paid enough attention to it or because the idea they came up with was too “early”. . During this period, it was very difficult to attract new funding from token sales, but classic funding was not always given to such ideas, so most of these startups failed.

The end of the crypto winter began roughly a year ago, when serious and at times conservative institutions began to enter the krito and blockchain market. Perhaps the first was Facebook, which, although it had banned posts and ads in this direction for years, still came up with its own blockchain and crypto platform. Facebook was followed by various institutionalized and controlled implementations by Swiss banks and, from 2020, by some German banks and the ICO, such as IEO (Initial Exchange Offering) or SAFT (Simple Agreement for Future Tokens), with moderate success for the time being. Last but not least, the European Union is testing its own blockchain platform, and J.P. Morgan, calling Bitcoin a scam for years, is launching its own Bitcoin-based investment services.

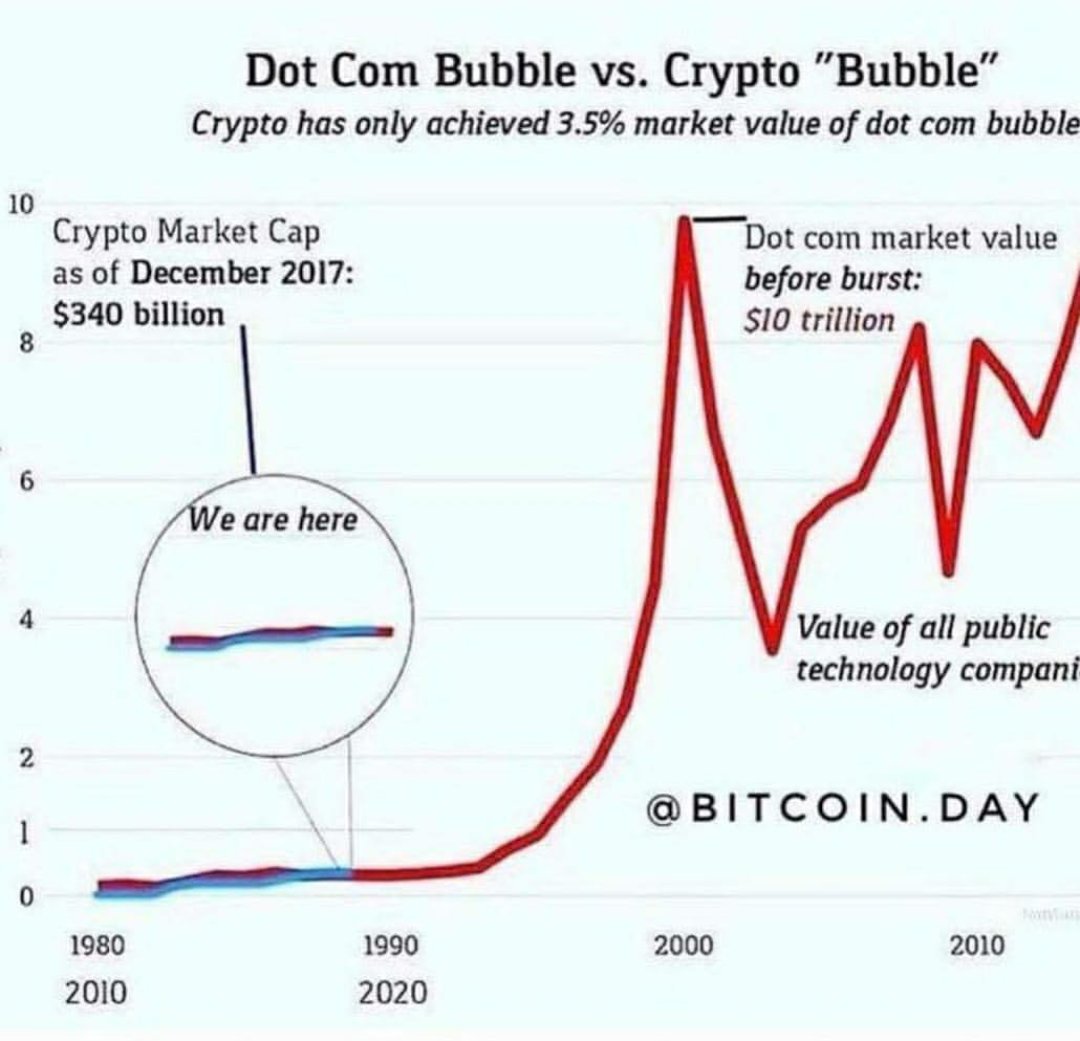

We might say a little biasedly that the future of technology is not in question, but individual business implementations and specific market developments already do. The emergence of enterprise-level institutions in the market does not preclude the emergence of similar bubbles at all, and in some cases they may even be much larger than in 2018, given that the capitalization of the entire crypto market is still far below the size of the dotcom bubble.