Link: Tokenized zero knowledge machine learning and its applications

...by Daniel Szego

|

| |

|

"On a long enough timeline we will all become Satoshi Nakamoto.."

|

|

|

Daniel Szego

|

Showing posts with label token. Show all posts

Showing posts with label token. Show all posts

Saturday, January 18, 2025

Wednesday, March 15, 2023

Tokenization in Financial Services presentation

Tokenization in Financial Services, presentation at the Hyperledger financial markets special interest group is available.

An introduction to tokenized financial securities

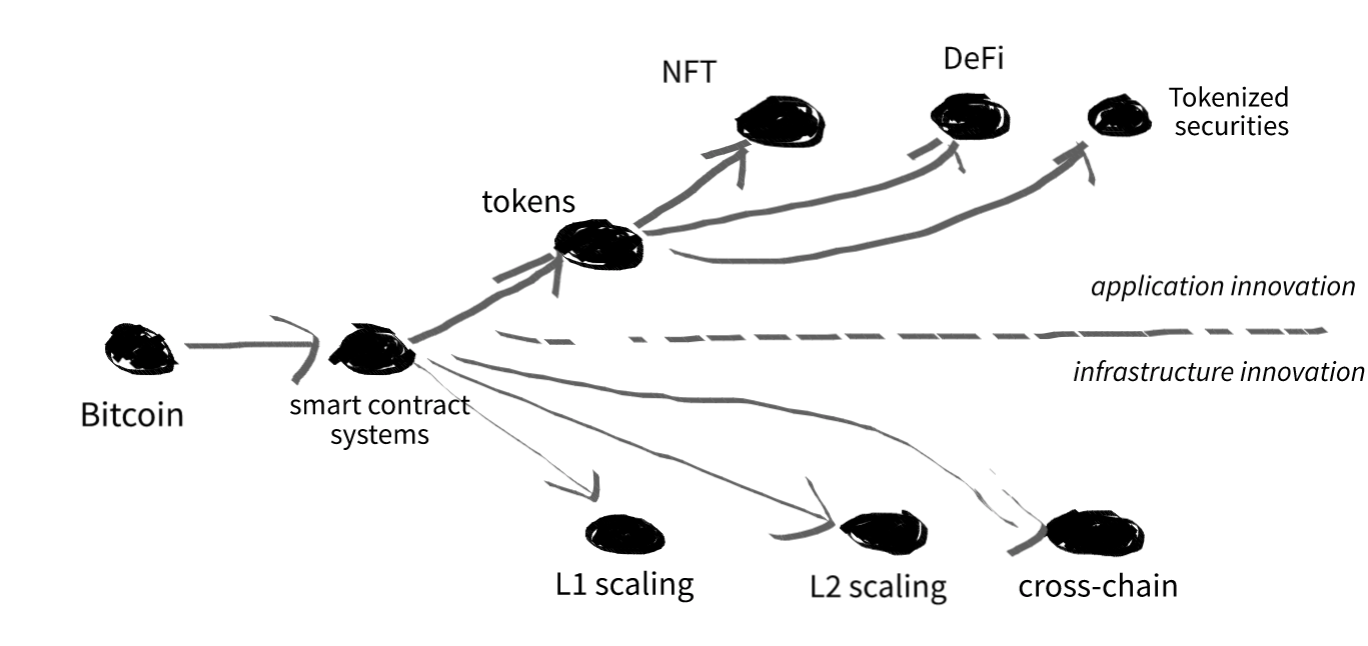

Current trends in blockchain research and development can be separated into two major categories. On the one hand, there is a very active research on the infrastructure side of these systems focusing mostly on scalability, privacy issues or cross-chain compatibility solutions of different distributed ledger platforms. Major approaches are layer 1 and layer 2 scaling possibilities. On the other hand, there is very active innovation on the application side as well having tokenization as a basic application level building block. Two of the probably well-known and perhaps over-hyped directions of the last 3 years are the NFT-s (non-fungible tokens) and DeFi (decentralized finance). As these approaches were mostly realized in the public and sometimes crypto-anarchist blockchain space, a lesser known direction on the regulated field is the trend of tokenized financial securities.

Tokenized financial securities are a new development in the financial industry that involves the use of blockchain technology to issue and manage securities in a digital form. These securities are represented by digital tokens that are secured and managed on a blockchain network. Tokenized financial securities are digital assets that represent ownership in a financial instrument, such as stocks, bonds, green-bonds, or real estate. They are issued through a process known as tokenization, which involves converting the ownership rights of an underlying asset into a digital token on a blockchain network. These tokens are then traded on digital asset exchanges or stored in digital wallets, just like other cryptocurrencies.

It is important to point out the difference between security tokens and tokenized securities. Security tokens are usually innovative and blockchain native tokens that are considered by the current legislation attempts under the same law as financial securities. It is especially difficult and controversial for native blockchain tokens and most of the decentralized finance (DeFi) protocols. However tokenized financial security considers classical financial securities that already exist for decades with well established regulation. These classical financial instruments are brought to blockchain protocols in a tokenized form.

One of the key benefits of tokenized financial securities is their potential to increase market liquidity. By enabling the fractional ownership of assets, tokenization allows investors to buy and sell smaller portions of assets, which can increase the number of potential buyers and sellers in a market. This can lead to more efficient price discovery and lower transaction costs. Tokenization also offers greater transparency and security than traditional financial securities. Since tokenized securities are recorded on a blockchain network, all transactions are transparent and immutable. This means that investors can easily track the ownership and transfer of securities, reducing the risk of fraud and errors. Furthermore, tokenization can help to reduce the cost and complexity of issuing and managing financial securities. By using blockchain technology, the process of issuing and trading securities can be streamlined, reducing the need for intermediaries and lowering transaction costs. This can make it easier and cheaper for companies to raise capital, and for investors to access a wider range of investment opportunities.

However, there are also challenges and potential risks associated with tokenized financial securities. One of the main challenges is the lack of regulatory clarity around these new digital assets. While some countries have established regulatory frameworks for digital assets, many others have not, creating uncertainty and potential legal risks for investors and issuers. Additionally, the adoption of tokenized financial securities is still in its early stages, and there are concerns around the scalability and interoperability of blockchain networks. As more assets are tokenized and traded on these networks, there is a risk that they may become congested, leading to slower transaction times and higher costs.

Major categories for tokenized financial securities are:

- Tokenized stocks: Companies can issue tokenized versions of their stocks, allowing investors to buy and sell them on a blockchain-based platform. This provides a more efficient and transparent way to trade stocks, with lower transaction fees and faster settlement times.

- Tokenized bonds: Similar to tokenized stocks, companies can issue tokenized versions of their bonds, allowing investors to purchase fractional ownership of the bond. This provides a more accessible way for investors to participate in the bond market.

- Tokenized real estate: Real estate assets can be tokenized, allowing investors to buy and sell fractional ownership of the property. This provides a more liquid and transparent way to invest in real estate, with lower transaction fees and faster settlement times. One interesting and perhaps controversial direction might be the tokenization of mortgage back securities (MBS) or asset backed securities (ABS) providing a more transparent and possible risk-free approach for the whole industry

- Tokenized commodities: Commodities like gold and silver can be tokenized, allowing investors to buy and sell fractional ownership of the asset. This provides a more accessible way for investors to participate in the commodity market.

- Tokenized funds: Investment funds can issue tokens representing ownership in the fund, allowing investors to buy and sell fractional ownership. This provides a more efficient and transparent way to invest in funds, with lower fees and faster settlement times.

In the international examples, we can already find several initiatives for the successful issuance of tokenized securities. An example of this is the tokenization of the BNP Paribas (BNPP) green bond. In the process, short-term tokens representing bonds were issued on the Ethereum blockchain. For the purchased tokens, the issuing institution undertook to officially convert them into the corresponding bond within 48 hours. Another example is Sygnum bank, which provides tokenized securities services to its customers. With its help, during a classic IPO, the issued shares can be listed on the Singapore Digital Exchange in parallel, in tokenized form. As a third example, it is perhaps worth mentioning Quadrant Biosciences, which sold 17% of its entire ownership in tokenized form. Another similar interesting direction is the tokenization of government securities, for which an innovative initiative will be launched in Israel at the beginning of next year, for example, with the support of the Tel Aviv Stock Exchange. Last but not least it is worth mentioning Siemens issuing a digital corporate bond in tokenized form just a couple of weeks ago.

Perhaps the question may arise as to how technically feasible a blockchain, especially public blockchain based securities issuance. The fact that most public blockchains are open, transparent, and accessible to everyone does not fit well with securities regulation. However, it is worth noting that, on the one hand, tokenization does not necessarily have to be implemented on an open blockchain platform, consortium platforms are conceivable, which can be regulated much better. On the other hand, even the most public and open platforms have token standards that can be used to create highly regulated tokens. Such a standard is, for example, ERC-1404, which enables, for example:

- know your token holder and KYC policies,

- linked to add KYC documents,

- whitelisting, blacklisting,

- blocking a token account,

- approving or prohibiting token transfer,

- “hard” coded rules: for example to prohibit trading between regions,

- token withdrawal,

- rights and roles (e.g. investor, administrator), etc.

In conclusion, tokenized financial securities represent an exciting new development in the financial industry, with the potential to increase market liquidity, transparency, and efficiency. However, there are also challenges and risks associated with this new technology, including regulatory uncertainty and scalability issues. As the adoption of tokenized financial securities continues to grow, it will be important for regulators, investors, and issuers to work together to ensure that these digital assets are safe, transparent, and accessible to all.

Tuesday, January 1, 2019

Notes on the future of token standards

Next generation of token standards will define cross-chain tokens, distributing efficiently the functionality between several blockchains or perhaps having even off-chain functionality. This will extend tokenomics and token based business models in the direction of multiply blockchains, or even blockchain and off-chain solutions. From a technological point of view, there is already several initiatives for realizing such a services, like Plazma, Loom network, Polkadot or Cosmos.

Tuesday, October 30, 2018

On the need of tokenized business and computational models.

Inevitable to most natural style of designing a blockchain application is to imagine a kind of a token model as a basic working mechanism. For that however we would need both the missing theory and practice as well to work with tokenized models, like inventing tokanized business models and/or tokenized computational architectures. Examples include but not limited to:

- tokenized data flow- tokenized Turing machine

- tokenized Neumann architecture

- tokenized accounting systems and tripple accounting

- tokenized business management

- tokenized business models

- tokenized business cooperation models

- tokenized machine learning

- tokenized AI

- ...

And last but not least we would need general frameworks to abstractly model and describe tokens and collaboration of tokens.

Monday, July 30, 2018

Cryptoeconomical attacks on Blockchain applications

It is actually a weird thing to identify attack surface for a blockchain based system. The major problem is that they are not purely software architectures, but rather complex systems containing both cryptography and software architecture components and elements based on economy. As a consequence "hacking" or "gaming" such a system is usually not purely a simple software engineering task. There can be the following types attacks:

- Classical attacks: like trying to break the cryptography, or exploiting an implementation vulnerabilities.

- Monetary attacks: these exploit the fact that a token or several tokens are actively traded on a couple of exchanges. As an example, pump-dump scheme or perhaps even shorting against a token or cryptocurrency can be regarded as such an attack. Sometimes such an attack is not clearly monetary, but for example is combined with a negative social media campaign.

- Certainly, there might be hybrid attacks as well, that try to exploit some system implementation errors combined with an economical "gaming". For such categories a new field of cybersecurity should be probably defined.

Wednesday, January 31, 2018

Computational and business models for tokenisation

As most blockchain platforms are built on different tokens and cryptoassets it can be foreseen that most new state of the art blockchain end user applications will be based from an architectural perspective on tokens. For this reason it is an interesting question how different computational models and IT architectures can be reformulated based on tokens. Among the others:

- How accounting can be built on tokens, similarly as triple accounting ?

- How workflows can be built up with the help of tokens ?

- How business processes can be formulated with the help of tokens ?

- How token based collaboration models can be set ?

- How data flow models can be defined by tokens ?

- How business models can be defined with the help of tokens ?

- How organisational structure can be defined on tokens ?

- How blockchain tokens and classical database or network technology can be integrated with each other ?

- How markets can be built on tokens ?

- How AI and machine learning can be built on tokens ?

- How markets can be built on tokens ?

- How AI and machine learning can be built on tokens ?

...

- What other kind of token based computational model can be imagined ?

Wednesday, January 10, 2018

Ethereum token with adjustable crypto-monetary policy with group of addresses

As we have mentioned in our previous blog there is a possibility and sometimes the need as well to create a token that has a actually a monetary base and an extended money supply as well that can be achieved in the most easy way with the help of a simple multiplicator value. However in certain situations, there might be the need to have something as multiply multiplication.

So let we further refine our model, let be M0 the monetary basis and M1 = M0 * m is an extended monetary supply where m is a multiplication number. Let we define an M2 refined and extended monetary supply in a way that:

- let G={g1, g2, ... gn} a set of groups, in a way that

- for each A={a1, a2, ... ak} possible addresses, there is maximum one gi group in which the address is member

- let |G|={|g1|,|g2|, ... |gn|} the number of addresses that are associated to a given group

- besides, let we have for each group a {m1, m2, ... mk} multiplicator value.

If so, we can define the M2 refined extended monetary supply:

M2 = M1 * Sumi (|ai| * mi) / Sumi (|ai|)

It is practically a measure for creating an average of different multiplicator values weighted by the size of the groups.

So let we further refine our model, let be M0 the monetary basis and M1 = M0 * m is an extended monetary supply where m is a multiplication number. Let we define an M2 refined and extended monetary supply in a way that:

- let G={g1, g2, ... gn} a set of groups, in a way that

- for each A={a1, a2, ... ak} possible addresses, there is maximum one gi group in which the address is member

- let |G|={|g1|,|g2|, ... |gn|} the number of addresses that are associated to a given group

- besides, let we have for each group a {m1, m2, ... mk} multiplicator value.

If so, we can define the M2 refined extended monetary supply:

M2 = M1 * Sumi (|ai| * mi) / Sumi (|ai|)

It is practically a measure for creating an average of different multiplicator values weighted by the size of the groups.

Tuesday, January 9, 2018

Minimal ERC20 token with adjustable monetary policy

As we have seen in the previous blog (Ethereum token with adjustable monetary policy), there might be a good idea to design a token with adjustable monetary supply, in a way that there is actually at least two token balances an M0 basic monetary supply and an M1 that is a dynamic multiplication of the basic monetary supply. The following code demonstrates a minimal implementation of such a token. For the first run as a simple sketch, without having some necessary elements for a live system, like Transfer event, safe match functions or token information fields

contract SimpleMonetaryToken {

mapping(address => uint256) m0Balances;

uint256 public monetaryMultiplicator = 110;

uint initialSupply = 10000;

uint initialSupply = 10000;

function SimpleMonetaryToken(){

m0Balances[msg.sender] = initialSupply;

}

function transfer(address _to, uint256 _m1Value) public returns

(bool) {

uint256 _m0Value = (_m1Value * 100) / monetaryMultiplicator;

require(_to != address(0));

require(_m0Value <= m0Balances[msg.sender]);

m0Balances[msg.sender] = m0Balances[msg.sender] - _m0Value;

m0Balances[_to] = m0Balances[_to] + _m0Value;

return true;

}

function balanceOf(address _owner) public view returns (uint256

balance) {

return (m0Balances[_owner] * monetaryMultiplicator) / 100;

}

}

Certainly, the structure should be further tested regarding the possible hackings or attacks. As an example division represents actually a rounding, so it might produces some inconsistencies or possible hackings. On the other hand, due to multiplications with 100, the overflow can be a critical issue.

Subscribe to:

Posts (Atom)